It was September, 38 years ago, when I decided to taste life as a California business journalist.

Related Articles

California housing to see stronger sales, rising prices in 2025, Realtors forecast

New California law gives tenants more time to respond to eviction notices

African American Cultural Center vision emerges in San Jose, adds homes

What is ‘chronic homelessness?’ 2 California lawmakers want to redefine it

Gov. Newsom signs bill limiting homebuyer sales contracts to 3 months

During all those years, one constant has risen above the noisy gyrations of the Golden State’s economy: how to keep lofty housing costs in check.

Almost everybody’s got an anecdote to portray this mess. My tale goes like this: In 1986, as a newly minted Californian, I bought a Santa Ana condo for $99,000. While I haven’t owned it for three decades, last year it sold for $600,000.

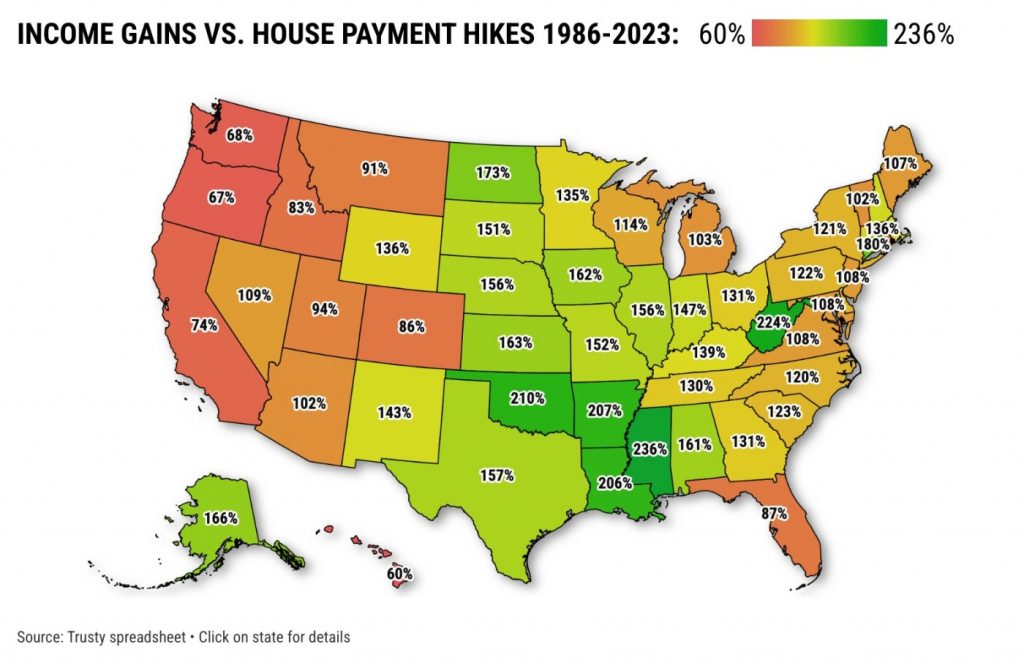

More broadly speaking, my trusty spreadsheet tells me that a typical California home in that same time span appreciated 612% – the fifth-biggest increase in the nation. Even adjusted for falling mortgage rates, the common house payment in the Golden State has jumped 415%.

Meanwhile, California incomes gained only 306% in the period. That payment-to-paycheck shortfall is the fourth-worst gap among the states.

So, if I’ve learned anything in my 38 years watching this grand affordability debate, it’s that making housing affordable isn’t rocket science. Yet, sadly, conflicted forces make solutions equally daunting.

Housing’s real challenge is that everybody’s got a “simple solution” to a multifaceted, multitrillion-dollar headache. There are no easy answers. It’s not Econ 101. “Build, baby, build” is only a partial cure.

You see, any fix will require a few people to lose a little so others can “win” in this game of housing affordability. That’s a tricky sell in this era of “what’s in it for me?”

To honor my years with the Orange County Register/Southern California News Group, and to help stir the pot, I offer up 38 housing questions – in random order, by the way – that contemplate California housing’s puzzle.

It’s not a quiz. Nor some wish list. Simply, food for thought. Enjoy!

1. How can housing transactions be modernized – and the cost dramatically lowered?

2. Are short-term rentals turning needed housing into less-needed vacation spots?

3. Housing “affordability” essentially means falling prices for purchases and renting, no?

4. Why can’t California simply start new cities as places for housing?

5. If we need a housing “free market” – why all the government support for real estate lending?

6. Why are “traffic” arguments used against housing developments but less so with retail projects?

7. Why do owners get tax breaks to buy second homes?

8. Do cities have too much control over how much, and what kind, of housing is built within its geography?

9. Are regulations requiring lenders to make sound mortgages part of the affordability challenge?

10. Why doesn’t government better fund the numerous rental assistance programs it started?

11. Will landlords developing “build-to-rent” complexes squeeze out house hunters seeking newly built homes?

12. How different would homebuying be if the government stopped its support for fixed-rate mortgages?

13. If the state is an insurance company for earthquake and fire risks, why not be a homebuilder, too?

14. Should landlords share rental data through third parties to “better” price and fill their apartments?

15. If California slashed its homebuilding environmental standards, what would really happen?

16. Can some sort of “rent control” be built that’s a win-win for tenants and landlords alike?

17. Imagine if California fought the “housing crisis” like it did wildfires?

18. Is housing’s problem too much money and too many incentives – rather than some grand shortage?

19. Should owners of commercial structures need an entire approval process to switch an old office or warehouse to housing?

20. The Federal Reserve owns $2 trillion in mortgages. When will the central bank end this homeowner subsidy?

21. Should foreigners be allowed to own US homes?

22. Does the Coastal Commission have too much say in housing built near the ocean?

23. Does new housing in fire-prone regions heighten risks – or actually help mitigate them?

24. When eggs get expensive, does anybody cheer? So why is housing appreciation or higher rents signs of a “good” market?

25. Is the huge share of home sales transacted through Realtors good or bad for consumers?

26. Should the government pay for the infrastructure supporting new housing – roads, sewers or schools – not the eventual owners of the residences?

27. Is the housing shortage really that big – and does that possible overstatement distract from other issues?

28. Does constructing luxury homes or apartments lower the price of all housing in a market?

29. Roughly half of all new homes nationwide are built by a handful of giant corporations. Should you be worried?

30. With an aging population, who in 20-30 years will be buying the homes being sold today – or the apartments being rented?

31. Will California eventually have to choose between its agricultural industries or housing?

32. If buying a home is “the largest investment a family will make,” then why isn’t home-selling regulated like stocks or bonds?

33. Does tax deductibility of mortgage interest and property taxes help drive home prices higher?

34. Is the vast wealth within housing – the “American Dream” – the true enemy of affordability solutions?

35. Would more homes be built if Prop. 13 didn’t limit the property taxes cities can collect?

36. What government land can be deemed surplus and quickly sold to build new housing?

37. What is the difference between “greedy” developers and residents “protecting” their home values?

38. Are well-meaning grants to homebuyers part of the price problem?

Postscript

I grew up in New York City, so I’m a stock guy. And I’ll mention that the Standard & Poor’s 500-stock index grew 2,017% in these past 38 years. Yes, 21-fold.

That gain would have made the old Santa Ana condo hypothetically worth $2.1 million today.

And if you add dividends that corporations pay into that stock-price equation, the S&P 500’s grew 4,826% – or a $4.9 million condo. Yes, almost 50 times your investment.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]